From Strategy to Spade: Operationalising the UK's £725bn Infrastructure Decade

From Strategy to Spade: Operationalising the UK's £725bn Infrastructure Decade

The capital is there. The strategy is there. What is missing is the connective tissue between local ambition and institutional balance sheets — multiple investable pipelines threading SDS, Local Plans and Local Growth Plans to deliver the clarity and certainty that has been missing for decades.

The UK's 10-Year Infrastructure Strategy, published in June 2025, commits £725 billion of public capital and signals an appetite for £40–£50 billion of private investment a year into regulated sectors alone during the 2030s.

Read the headlines and it sounds like the deal flow problem is solved.

Speak to anyone trying to close a transaction at place level and a different picture emerges.

Institutional investors describe a market that is too fragmented to underwrite at scale. Local authorities describe a market where the only routes to capital still feel bespoke, slow and politically exposed. Mayoral Strategic Authorities sit in between — holding new powers, new pipelines and new pressure to convert manifesto commitments into shovel-ready outcomes inside a single political cycle.

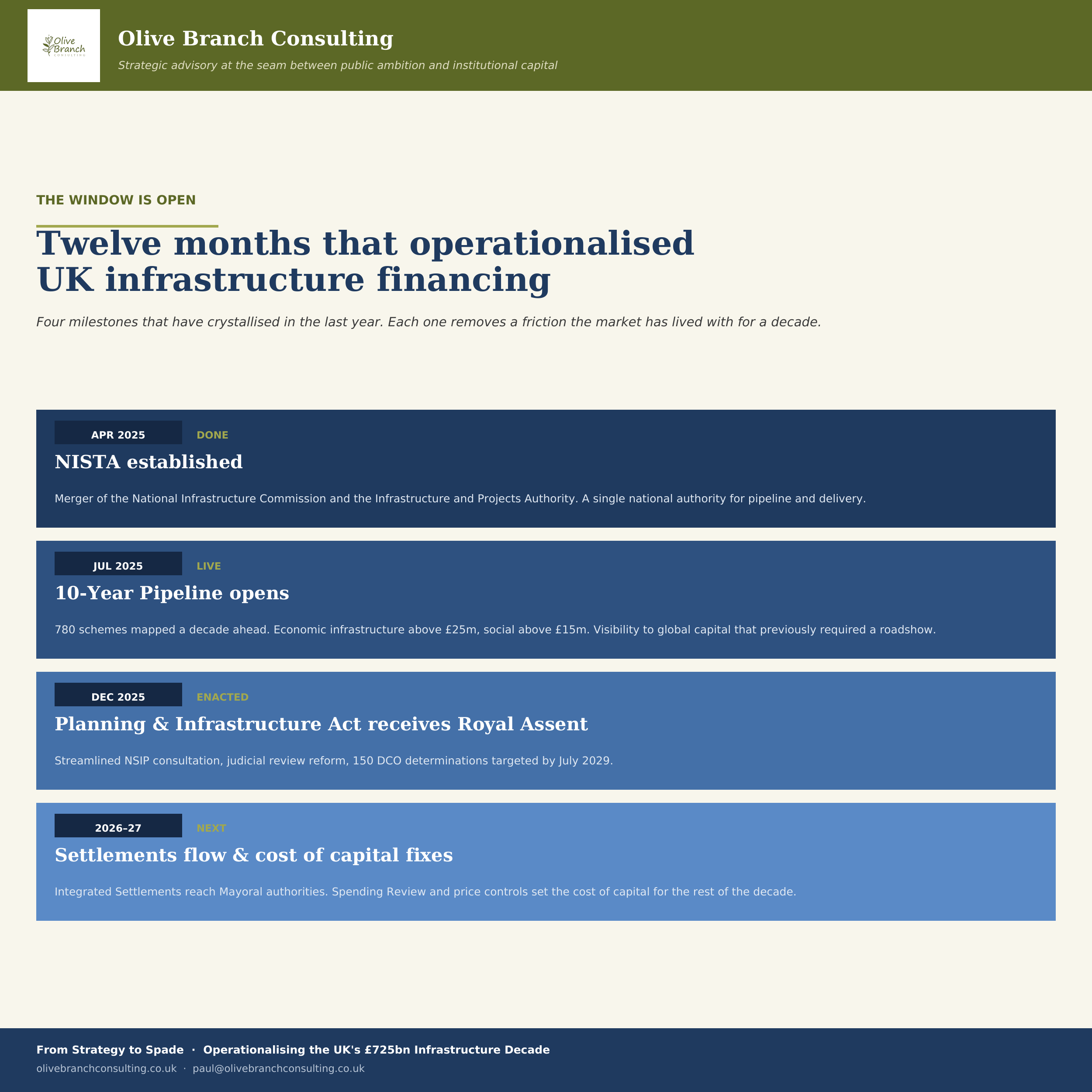

But over the last twelve months, the scaffolding has gone up. NISTA was formed in April 2025 from the merger of the NIC and the IPA. The 10-Year Infrastructure Pipeline went live in July 2025 with 780 schemes already mapped a decade ahead. The Planning and Infrastructure Act received Royal Assent in December 2025. Public Financial Institution firepower has been expanded by around 40% to over £137 billion.

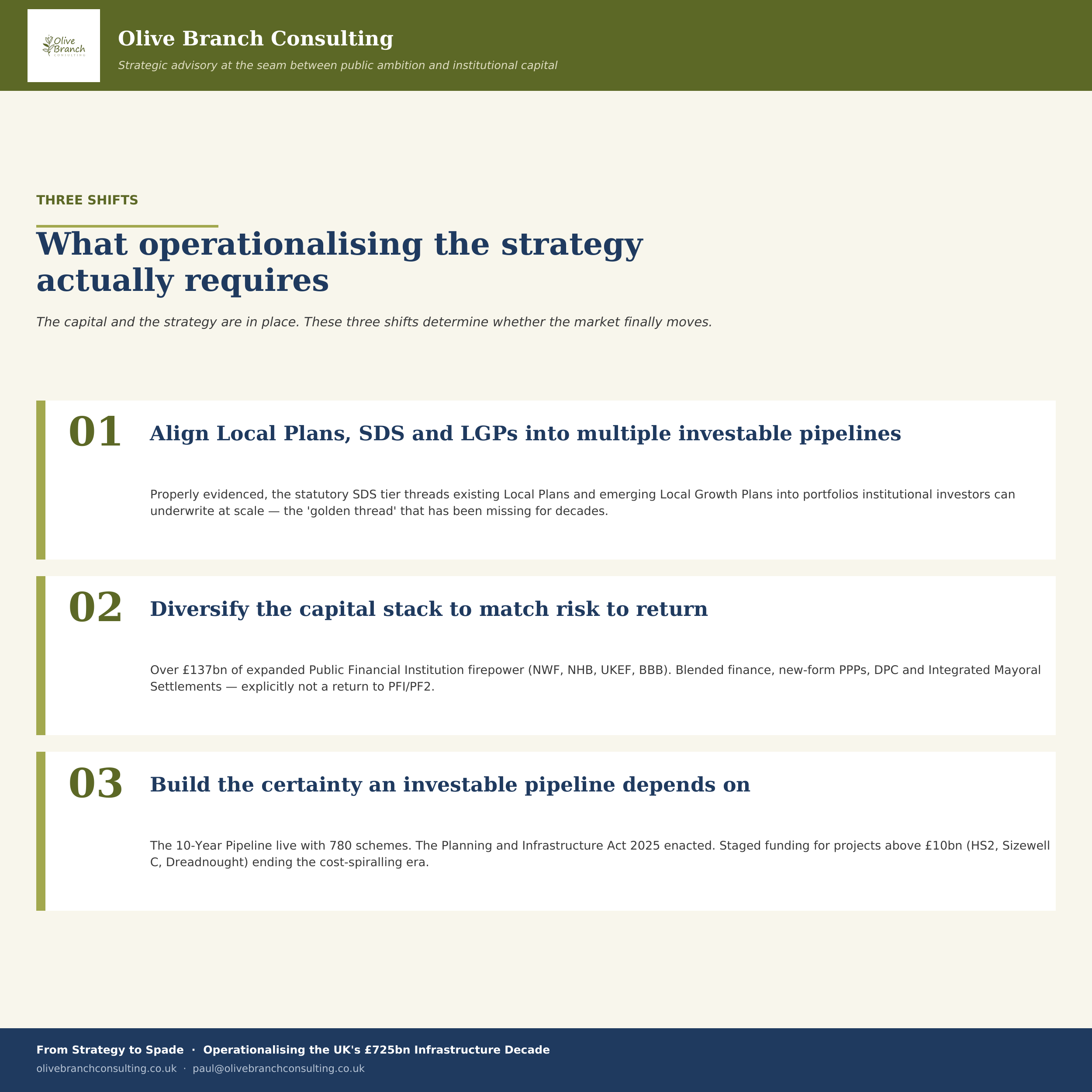

Three shifts now determine whether the next phase actually delivers the clarity the market has been waiting decades for.

1. Align Local Plans, SDS and LGPs into multiple investable pipelines

Local infrastructure has always struggled to attract patient capital. Not because the underlying assets are weak, but because the way they are presented is. A single junction upgrade, a single energy network reinforcement, a single regeneration parcel — each one too small to clear an institutional desk on its own.

The new statutory strategic planning tier is the first material change to this picture in a generation. Under the Planning and Infrastructure Act 2025, sub-regions now have a duty to prepare Spatial Development Strategies (SDS) coordinating housing, environmental and infrastructure delivery across local authority boundaries. Local Plans sit underneath them; Local Growth Plans (LGPs) sit alongside.

Properly evidenced and properly threaded, these documents become more than planning instruments — they become investment prospectuses.

Three practical moves earn outsized returns:

▸ Place-Based Business Cases. Bundle transport, housing and energy projects together and assess their complementary value. The only honest way to capture the upside of place.

▸ Place Coalitions. Convene local authorities, anchor employers, developers and LGPS pools as a standing investment partnership — not reconstituted for each transaction.

▸ Data foundations and digital integration. Standardised, digital, data-led approaches enable transparency, open API integrations and digital monitoring of impact and IRR — the basis for a marketplace of services that delivery and finance providers can actually use.

"A Local Growth Plan should be readable by a local member, a Whitehall sponsor and an institutional allocator — in the same afternoon, drawing the same conclusions."

2. Diversify the capital stack to match risk to return

The market still talks about infrastructure finance as if there is one cheque. There isn't.

Public Financial Institution firepower has been expanded by around 40% this Parliament to over £137 billion — with the National Wealth Fund (NWF) capitalised at £27.8 billion, the new National Housing Bank (NHB) at £16 billion, and growing UK Export Finance and British Business Bank capacity sitting alongside them. The question is no longer whether the public balance sheet can absorb early-stage risk — it is whether the deal architecture is in place to deploy it efficiently into multiple investable pipelines.

Three routes deserve more deliberate operationalisation:

▸ Blended finance at scale. Subordinated equity, guarantees and first-loss debt from PFIs alter project risk so LGPS pools and institutional investors can credibly deploy into higher-yielding, value-added strategies — battery storage, hydrogen transport, grid reinforcement, decarbonisation infrastructure.

▸ Targeted PPPs and Direct Procurement for Customers. New-form PPPs are being explored where revenue streams are clear — the HS2 Euston station DBFM model and public estate decarbonisation are early test beds. The Direct Procurement for Customers model demonstrated by the £3 billion Haweswater Aqueduct delivers the long-duration, inflation-linked cash flows core investors require. The 10-Year Strategy is explicit that this is not a return to PFI or PF2; the new instruments are bounded to specific revenue-bearing schemes with appropriate risk transfer and value-for-money tests.

▸ Integrated Mayoral Settlements as revenue backstops. Single, flexible settlements replace the fragmented grant landscape. For the first time, a Mayoral Strategic Authority can credibly enter long-term co-investments without re-baselining every fiscal event.

The unlock is sequencing. Public capital should be doing the work only public capital can do — taking early-stage risk, providing planning certainty, underwriting demand. Private capital should do what it does best — scale, discipline, long-duration matching. Where projects are stuck, that division of labour is almost always muddled.

"The state has done its part on capacity — over £137 billion of expanded PFI firepower. The question is whether the deal architecture is in place to deploy it efficiently."

3. Build the certainty an investable pipeline depends on

Investors, supply chain and skills providers all commit on the strength of pipeline visibility. Three things now determine whether the strategy finally delivers the clarity the market has been waiting decades for.

▸ The NISTA 10-Year Pipeline as a national shop window. Launched July 2025 with 780 schemes mapped a decade ahead — economic infrastructure above £25m, social infrastructure above £15m. Local authorities arriving with mature priorities gain visibility to global capital that previously required a roadshow. Those that don't will find themselves invisible inside a transparent system.

▸ Resolving the pre-construction bottleneck. The Planning and Infrastructure Act 2025 is the structural fix — streamlined NSIP consultation, judicial review reform (paper permission stage removed for NSIPs, "Totally Without Merit" cases barred from Court of Appeal reconsideration), and a target to determine 150 DCO applications by July 2029, nearly tripling the previous Parliament's output. The faster operational win is aligning SDS and LGP evidence with what is already in development plan pipelines, so 'early wins' become visible to the finance sector inside a market cycle rather than a political one.

▸ Strategic governance for mega projects. The staged, incremental funding approach mandated for projects above £10 billion is the most important governance change in a decade — currently scoped to HS2, Sizewell C and Dreadnought. Fixed capital envelopes granted only once design and risk are mature should bring the HS2 era of cost-spiralling to a close.

"Local authorities that arrive with mature priorities gain visibility to global capital. Those that don't will find themselves invisible inside a transparent system."

The window is open

The last twelve months have done more to operationalise UK infrastructure financing than the previous decade combined.

NISTA is established. The 10-Year Pipeline is live with 780 schemes. The Planning and Infrastructure Act 2025 has received Royal Assent. PFI firepower has been expanded by ~40% to over £137 billion. SDS duties are crystallising. Integrated Settlements are flowing to Mayoral authorities. The 2025 Spending Review and the next set of regulated price controls will set the cost of capital expectations for the rest of the decade.

Authorities that arrive at the end of 2027 with a properly evidenced Spatial Development Strategy, a Strategic Infrastructure Plan, a defined Place Coalition and a portfolio threaded through their Local Plans and Local Growth Plans will be operating in a different market to those that don't.

They will be the institutions finally bringing decades of investment uncertainty to a close.

The capital cost of being slow will not be subtle.

At Olive Branch Consulting we work at the seam between public ambition and institutional capital — Strategic Infrastructure Plans, aligned pipeline development, Place Coalition design, blended finance structuring with PFIs and LGPS pools, NISTA pipeline readiness, mega-project governance reviews.

If any of this resonates, I'd welcome the conversation. DMs open.

📧 paul@olivebranchconsulting.co.uk 🌐 olivebranchconsulting.co.uk

Sources: HM Treasury (10-Year Infrastructure Strategy, June 2025; Spending Review 2025); GOV.UK announcements on NISTA, the 10-Year Pipeline and the Planning and Infrastructure Act 2025; the National Wealth Fund and Homes England (National Housing Bank); the Department for Transport on HS2 Euston procurement.

#Infrastructure #PlaceBasedInvestment #PublicPrivatePartnership #BlendedFinance #LGPS #SpatialPlanning #NISTA