The Devolved UK: The Levers Are Already Open

The levers are open, but three frictions stand between them and "good growth". A case for rewiring local, regional and central government as one system.

A response to The Rest Is Politics, ep.548, and a note to anyone in Whitehall or a combined authority who has to turn "good growth in every postcode" into something that actually gets built.

The argument in one breath

On their 30 June episode, Rory Stewart and Alastair Campbell gave Andy Burnham's first major speech the most serious hearing it has had anywhere, and I think they were right about almost everything they conceded while being only half-right about the one thing that matters most. Their conclusion, in essence, was that Burnham has handcuffed himself: with no rise in income tax, national insurance, corporation tax or VAT, and the fiscal rules held, there is no real money for the "biggest council housing programme since the war," which leaves, as Rory sees it, only the radical deregulation of planning that he doubts Burnham will ever deliver. Viewed through the status-quo lens that is a fair pessimism, but it is only half-aimed, because while it is quite right that money binds, it is wrong to assume the tax rate is the only place money and delivery capacity enter the picture.

What the episode never quite reached is that, over the last twelve months, Parliament has quietly unlocked most of the functional toolkit devolved government actually needs, and that much of it can be operated without touching a single tax rate. An open lever is not the same thing as accelerated growth or a delivered home, though, and three frictions sit in the gap between the two: most of the levers still score to the public balance sheet, the institutional capital everyone gestures at will not go where the mission needs it, and the delivery capacity to pull any of it has been hollowed out and is now being eaten alive by reorganisation. However the caveat is not that the levers make the problem disappear, but that they raise the ceiling on what a given amount of money and capacity can deliver, and the four moves that follow are an attempt to focus the mind on what we can, and should, actually be doing about that.

Two devolutions, and the one the debate keeps missing

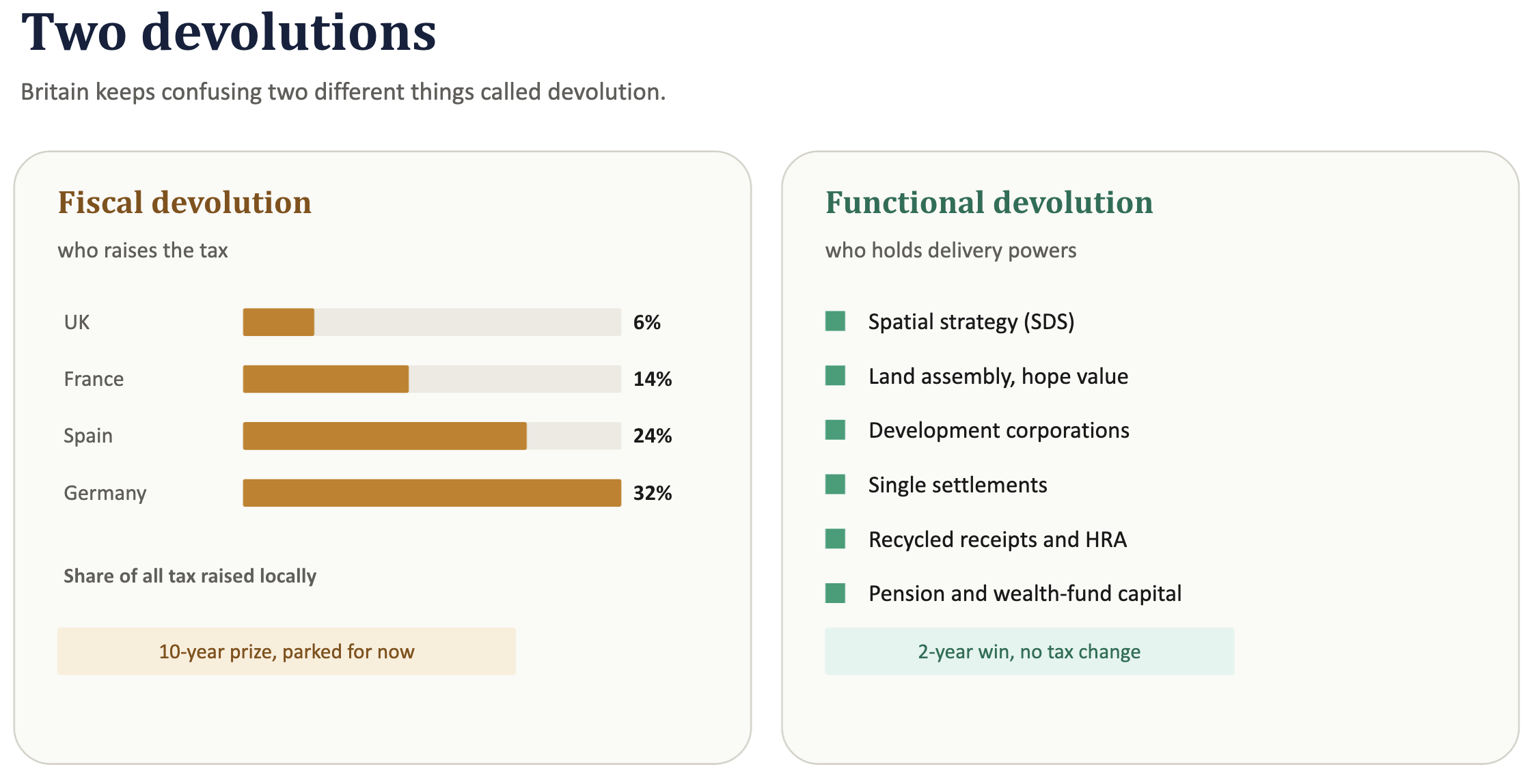

Part of the trouble is that we use one word, devolution, for two quite different things, and the housing exchange on the podcast fell straight into the gap between them.

The first is fiscal devolution, by which I mean which tier of government raises and keeps the tax, and here Britain really is an outlier: on Campbell's own figures roughly 6% of tax is raised locally against 14% in France, 24% in Spain and 32% in federal Germany. Closing that gap is the ten-year prize, and Burnham has chosen not to pick the fight yet, but it is worth being clear about why, because two arguments keep getting run together. Devolution is parked by Treasury control, by the politics of redistributing between richer and poorer places, and by the sheer difficulty of standing up any new local tax, and it is not parked by the four-tax pledge. That pledge, the promise not to raise the rates of income tax, national insurance, VAT or corporation tax, which between them bring in about two-thirds of all revenue, is a statement about how much the centre can raise nationally; it is Rory's "handcuffs," and it belongs to the money argument I come to under the frictions. Fiscal devolution sits on a different axis altogether, the level at which tax is levied, and you can hand a locality real power, whether a share of income tax, retained business rates or a local levy, without touching a single national rate. Conflating the two is exactly how people talk themselves into believing devolution is blocked by a tax promise when it is really blocked by the centre's reluctance to let go.

The second is functional devolution, meaning who holds the powers to plan, assemble land, build, connect infrastructure and spend a settlement against local outcomes, and this is the near-term game precisely because it is almost entirely separable from tax. When the podcast treated "no new taxes" as if it were the same thing as "no delivery capacity," that was the load-bearing error of the whole episode, and once you see it the mood genuinely lifts, because the two-year win and the ten-year prize turn out to be different battles that can be fought on different timelines. The right sequence is not to win the fiscal argument and only then deliver, but to operate the functional levers now, show that they work, and let visible delivery earn the mandate for the fiscal settlement later.

The toolkit that is already open

The claim that Burnham has no money levers for housing only holds if you assume housing is paid for from Exchequer grant or general borrowing and nothing else, and it is not. The Housing Revenue Account borrowing cap went in 2018, so stock-holding authorities can now borrow against their expected rental income under the Prudential Code; councils keep 100% of Right to Buy receipts and can pair them with grant to build replacements; Homes England has stood up a National Housing Bank to unlock investment at scale; and the Planning and Infrastructure Act 2025 has extended the power to strip "hope value" out of compulsory-purchase compensation for affordable and social housing, applied scheme by scheme through directions rather than as a blanket abolition and carrying real human-rights risk that will need watching. Put borrowing capacity, recycled capital, an investment bank and cheaper land assembly together and you have a demanding delivery stack, which is a very different thing from "no levers."

On planning, Rory framed the only remaining route as radical deregulation, but that is the wrong word for the most important thing that has already happened, because the same Act created a statutory Spatial Development Strategy duty at the sub-regional level, removed the old duty to cooperate, and put in its place a single strategic plan that sets, by law, the amount and distribution of housing along with climate policy, health and strategic infrastructure. That is not a bonfire of rules but the discipline of setting the contested numbers once, at the scale where they can genuinely be reconciled and with an examined evidence base behind them, rather than watching them die site by site in district committees. Alongside it sit delivery vehicles with real teeth, since Mayoral Development Corporations can hold land and compulsory-purchase powers while Mayoral Development Orders grant planning consent, and taken together they let a single accountable body assemble the land, consent the scheme and de-risk the site, which is how you build at scale in practice rather than by a minister exhorting the market.

And the capital is there, actively looking for exactly this sort of thing, because the fiscal rules and the bond markets are better understood as a design parameter that pushes you toward crowding in private and institutional money than as a wall that keeps it out. The National Wealth Fund exists to de-risk through first-loss layers and guarantees, aiming at something like three private pounds for every public pound (verify capitalisation, around £27.8bn), while the LGPS "Fit for the Future" reforms now require pools to set and report a local-investment target, with a 5% allocation on the order of £20bn today. This is patient capital, sitting under a fiduciary duty and mandated to hunt for investable local pipelines, which is why the binding constraint is not really the absence of money at all but the absence of bankable propositions for that money to buy. That last point is the one I would nail to the door.

Visible is not the same as investable

Rory and Alastair handed themselves the single most important fact in the episode and then declined to draw the conclusion from it. The Public First work they cited found that roughly £19bn of place funding, across the towns fund, shared prosperity, levelling-up and pride-in-place, went into the least affluent areas, that Hartlepool received something like £974 a head since 2016 against a pound or three a head for London councils, that a great deal was genuinely built, and that for all of it the politics moved not at all, since if anything the more money an area received the more likely it was to vote Reform or Restore.

The lazy reading is that investing in places simply does not work, but the correct one is that centrally-chosen, short-horizon, project-by-project money, dropped on a place that has no agency and no revenue stake, does not work. A place can be made visible, with a prospectus and a pipeline and a ribbon to cut, without ever being made investable, which needs a creditworthy payer, real recurring revenue and a deliverable consent, and that distinction is the intellectual core of the Burnham proposition, stronger than he has yet made it himself. "Not just giving money" is the hard lesson of the £19bn, and the remedy is not more money or less but money routed through institutions that own the outcome, hold a revenue stake and can recycle capital, so that a public pound pulls in private capital and then comes back round to be spent again. That is ownership rather than allocation, and it can largely be built without a rate change, though, as the next section makes plain, not without a cost to the public balance sheet.

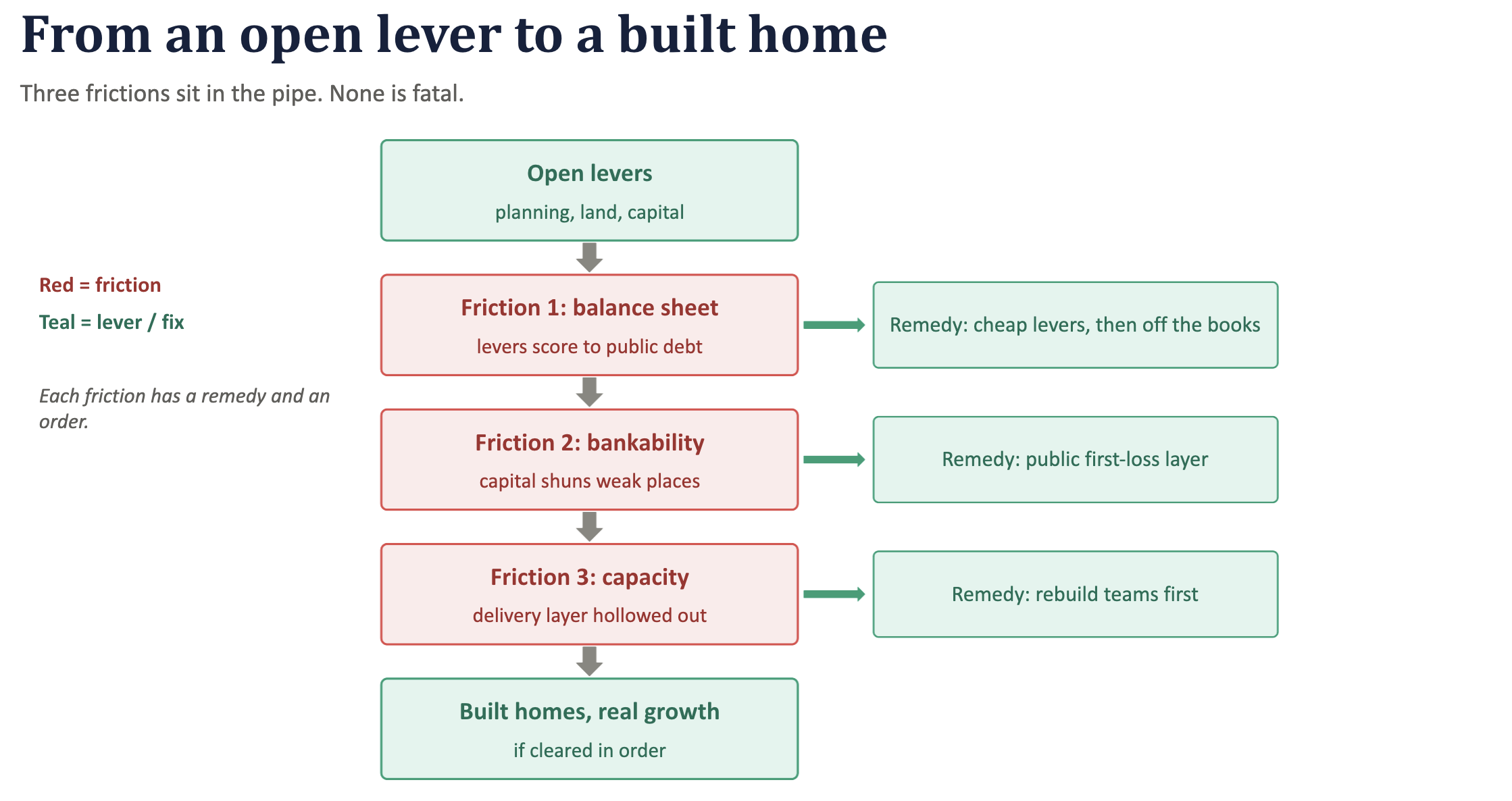

The three frictions between an open lever and delivering growth

Being honest about the toolkit means being just as honest that an open lever is not a delivered outcome, and since a good Treasury official could puncture the frictionless version of this argument inside a single meeting, it is worth making their case for them; there are three frictions, and each comes with a remedy and a sequence rather than a wish.

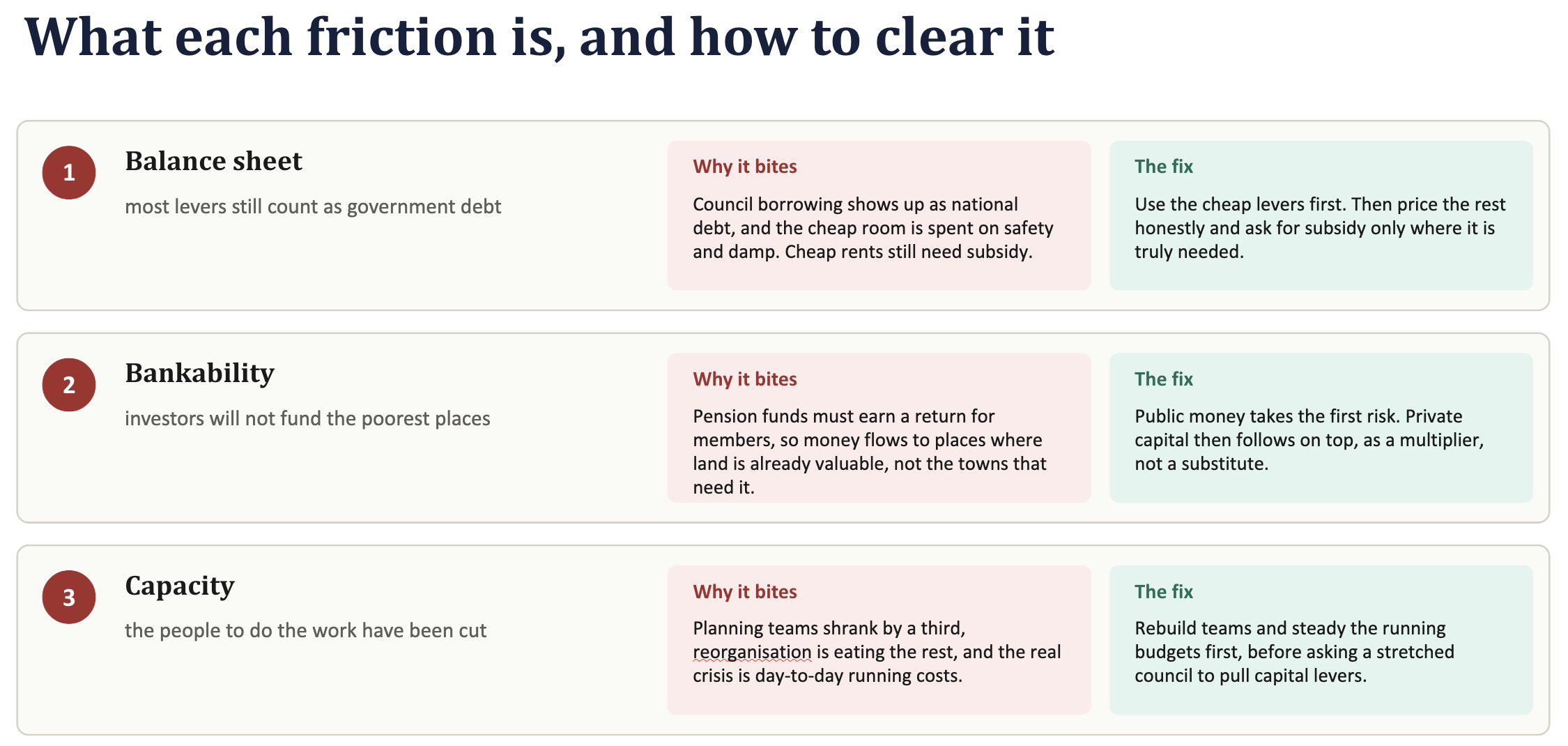

Friction 1

The first, and the strongest, is that most of the levers still land on the public balance sheet, because Housing Revenue Account borrowing counts to Public Sector Net Debt, its headroom is already largely spoken for by decarbonisation and building-safety and damp liabilities on rents that were cut between 2016 and 2019, development-corporation borrowing scores too, and since the National Housing Bank and the National Wealth Fund lend rather than grant while sub-market rent will not service commercial debt, social housing at scale still needs subsidy. So "no tax rise needed" cannot mean "no fiscal consequence"; it means the consequence shows up as debt rather than as a change in the rate, which is a real constraint and not a loophole, and the remedy is a sequence: exhaust the genuinely low-scoring levers first, which are planning at scale, land assembly that captures uplift and receipt recycling, price the balance-sheet cost of the rest honestly, and then put whatever subsidy is still needed on the table openly rather than disguised as a free lever.

That cheapest lever is easily misread, though, so it is worth a word, because when I say land assembly that captures uplift I do not mean another turn of the section 106 screw. Skimming a contribution off someone else's scheme is the tired pond, negotiated away on viability, pro-cyclical, and thinnest in exactly the low-value places the mission is aimed at, whereas the method that earns its place is the opposite one, where the public body assembles the land itself, buys it closer to existing-use value now that hope-value reform allows it, grants its own consent and captures the whole farmland-to-residential uplift to recycle, which is the New Towns and development-corporation model rather than a developer contribution. The limit is the same every time, because capture is cheap precisely in that it self-funds from uplift and uplift is the one thing the weakest places do not have, so in a strong market it recycles and barely touches the balance sheet while in a low-value town the sums simply do not close and you are back to grant, which is exactly why the sequence has to end with the honest subsidy ask for the places the pond cannot reach.

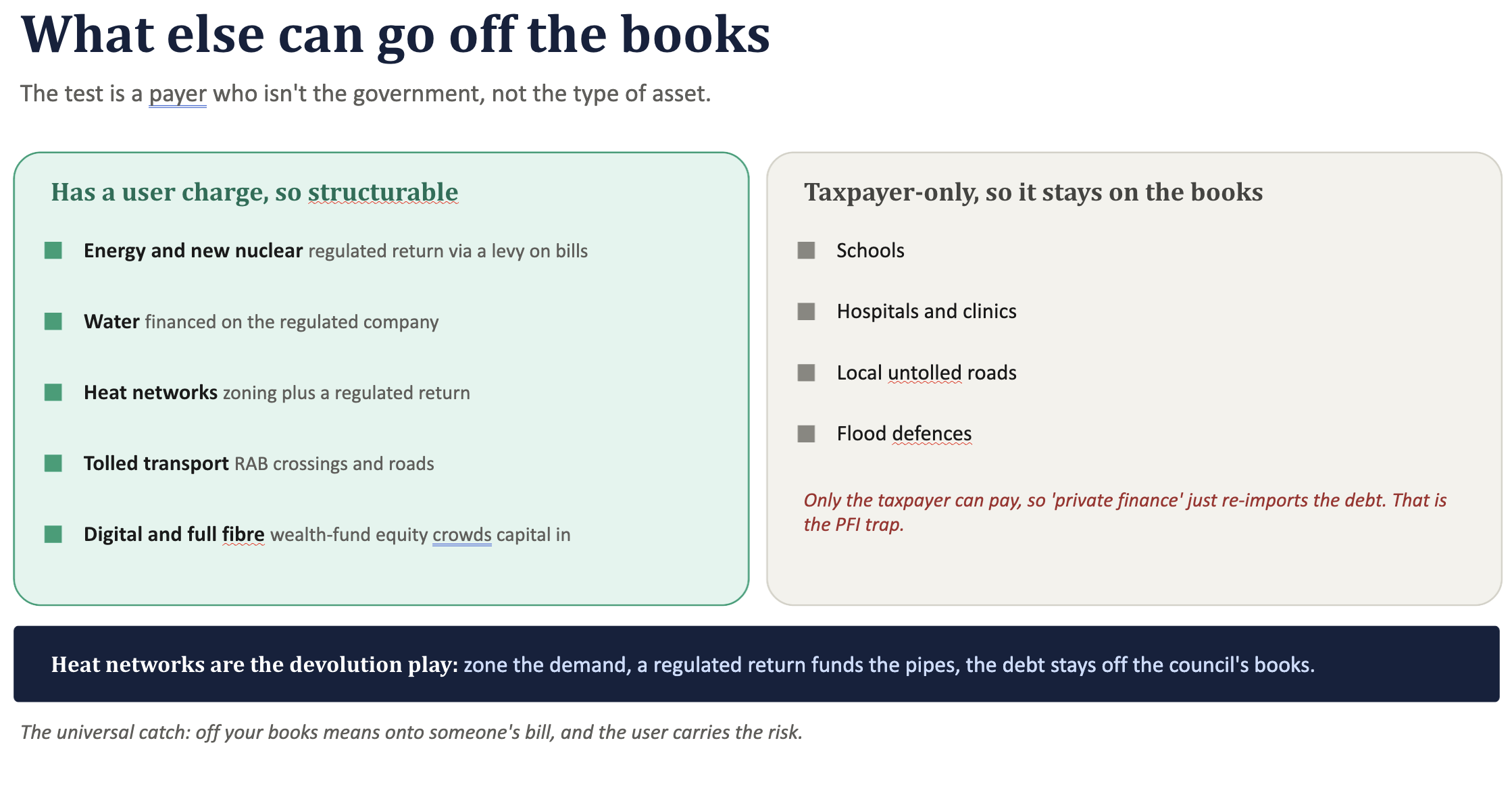

There is a sharper move sitting inside this first friction, and it is the most double-edged of the lot, because part of the delivery can genuinely be taken off the balance sheet. The fiscal rule now targets Public Sector Net Financial Liabilities rather than net debt, so equity, loans and guarantees routed through the National Wealth Fund already score far more lightly than grant, and classification itself is structural rather than rhetorical, since the ONS market-body test turns on whether a vehicle covers more than half its costs from sales and whether government exerts significant and specific control over it; pass the first and loosen the second and the vehicle becomes private, its borrowing off the public books, exactly as happened when housing associations were reclassified into the public sector in 2015 and then, once the 2017 deregulation stripped out ministerial controls, moved back out again taking roughly £66bn of debt with them. So a market-facing housing company, development corporation or regulated-asset-base structure can carry real delivery off the constraint, but the price is fiduciary rather than an accounting trick, because you buy that balance-sheet space with control, since you cannot both direct a vehicle and de-consolidate it, and with mission, since the test rewards cost-covering rents rather than the deepest social rent, and you create no new resources at all, only relocate where the debt is recorded. This reaches well beyond housing, since the real test is whether there is a payer who is not the government, so anything with a user charge can in principle go off the books, from energy and new nuclear on a regulated-asset-base levy (Sizewell C reached that point in 2025) through water, tolled transport, heat networks and full-fibre, while the line you cannot cross is its mirror image, because schools, hospitals, untolled roads and flood defence have only the taxpayer to pay and dressing them up as private finance simply re-imports the liability, which is the PFI lesson we ought not to need to relearn.

Friction 2

The second friction is that the capital is real but it will not go where the mission needs it, since institutional money is looking for investable, de-risked, yielding assets and a pension fund cannot, under its fiduciary duty, buy sub-hurdle deals for reasons of local loyalty, because the LGPS "5% local" is a target range and not a mandate to lose members' money. Infrastructure equity wants the double-digit greenfield returns that regeneration in a low-value town will not clear unaided, and land value capture only really bites where values are already high, which is the greater South East and not the postcodes the mission is named after, so the pipeline ends up visible but not bankable and making it bankable means public subsidy or risk-bearing, which loops you straight back to the first friction. The remedy is to stop treating institutional capital as a substitute for public money and start treating it as a multiplier on a public first-loss or revenue-floor layer, with the National Wealth Fund taking the risk institutional capital cannot, and to be geographically honest about the rest, using the market-facing levers where the market actually exists and accepting that the weakest places need grant and capability rather than clever structuring.

Friction 3

The third friction is that execution is the slowest variable of all, and reorganisation is currently eating it, because it can be fixed only slowly and at the moment it is going backwards, with planning teams down by something like a quarter to a third after a decade of austerity and Local Government Reorganisation consuming exactly the management bandwidth the levers require, the very bodies that will hold the spatial-strategy duty being abolished, merged or created mid-flight through 2027 and 2028. You cannot bolt delivery machinery onto a moving org chart, and it does not help that the binding crisis in local government is a revenue crisis rather than a capital one, with adult social care, special educational needs and temporary accommodation driving section 114 notices while every lever I have described sits on the capital side of the ledger, so the remedy is to treat capacity as the first-order deliverable rather than an afterthought, protecting and rebuilding the planning and commissioning teams, sequencing the capital levers behind the LGR vesting dates so that you are not asking a dissolving council to stand up a development corporation, and pairing every capital lever with the revenue and skills to run whatever it builds. Capacity and revenue stabilisation have to come first, or the levers just pull against empty hands; and while none of the three frictions is fatal, naming them changes the claim honestly, because the levers do not remove the need for money and capacity so much as raise the ceiling on what a given amount of each can deliver.

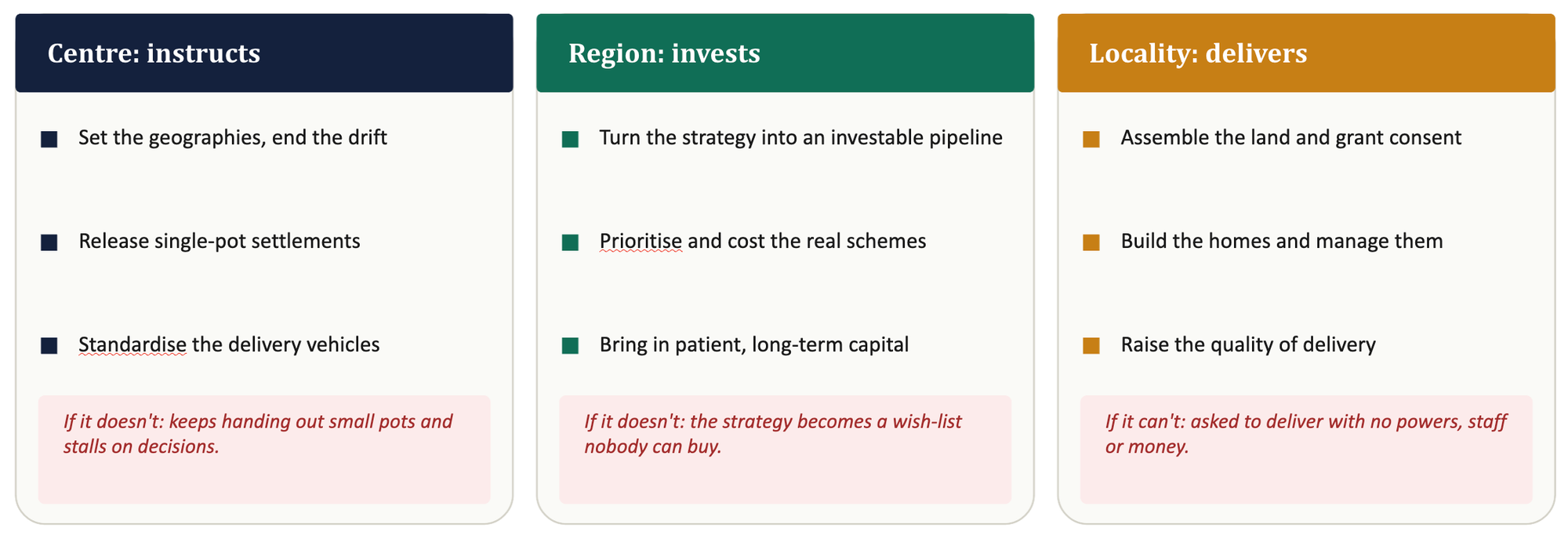

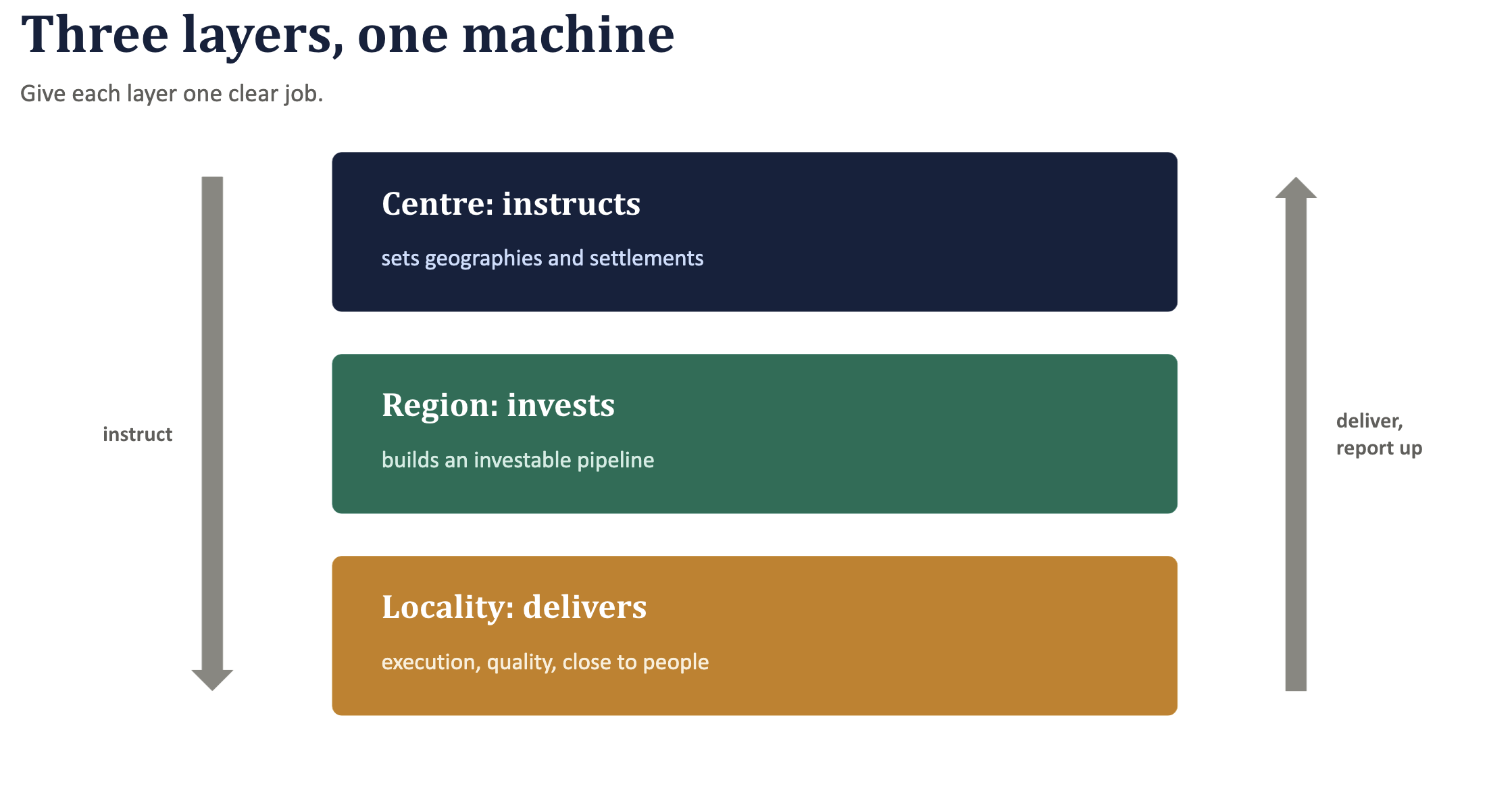

One system, and where the wiring lives

Step back and the real prize comes into view, which is that we do not have a local government problem and a regional government problem and a central government problem, we have one system that is badly wired, in which the centre hoards the money and the decisions, the region holds the mandate but not the levers, and the locality has the knowledge but neither, and almost every pathology the podcast identified, the £19bn that changed nothing, the housing targets that will be missed, the collaboration parliament will corrode, follows from that single miswiring. Rewiring it starts with being clear about what each layer is for: the centre should do far less commissioning and far more instructing, setting the geographies, releasing the settlements, standardising the vehicles and holding the outcomes framework before getting out of the delivery business, because its deepest pathology is an indecision that forces local actors to choose and thereby exposes their splits, and the cure is almost always to instruct, to convert a contested local choice into a settled national parameter; the region, the strategic authority, is where strategy and investment are meant to meet, so its spatial development strategy ought to be a costed, prioritised and genuinely investable pipeline rather than a scaled-up local plan, which shifts the question from "what do we want to build" to "who is paying, and what exactly are we asking to be paid for"; and the locality is where quality is won or lost, on the landings and in the classrooms and on the sites, which is why Rory's best point of the whole episode, that fixing Britain is the slow and unglamorous business of raising execution quality over years, is really an argument for proximity rather than against it.

Which is precisely where Burnham's "Number 10 North" finally earns its keep, and why I think the podcast was too quick to wave it away, because "one system" stays an abstraction until you can say where the wiring physically lives, who it is that actually holds the shared data, the standard vehicles, the single settlement and the digital capability. As a building in Manchester, with the obligatory reminder that the north does not end at the M60, it really is worth very little, so the hosts were right to be sceptical of the branding, but strip the nameplate off and what is left is the nerve centre that runs the plumbing, potentially the most important machinery-of-government reform in a generation, worth having to the exact extent that it holds four functions. It should hold a single data and outcomes spine, so that a stretched authority reports the same reality once rather than four times over and the centre's oversight becomes real-time rather than retrospective; standardised delivery vehicles as off-the-shelf templates, so that a mayor can stand a corporation up in months instead of commissioning a governance review from first principles; the single-settlement machinery, the single-pot funding against outcomes that is really Total Place reborn, so that mayors spend against local outcomes instead of bidding year after humiliating year into fifty competitive pots; and a capability layer, which is where the AI question the hosts raised actually bites, since AI and shared digital services are bandwidth for the stretched teams doing planning determination and casework and monitoring, and standardising that across forty authorities is how you begin to close the very execution gap Rory rightly says is everything. A nerve centre that is only a nameplate will fail, and the podcast would be right to mock it, whereas one that holds those four functions turns the narrative into consented, financed, built reality, so wire the three layers together on the simple rule that the centre instructs, the region invests and the locality delivers, and you have a system that can actually convert ambition into homes; leave it miswired and you get another £19bn and another disappointed decade.

What this means for the Burnham moment

The honest scorecard, then, is that they were right about the tax handcuffs, right that levelling-up money bought no loyalty, right that execution is the whole game and right to distrust imported models, and on the money they were rather more right than the frictionless version of my own argument allowed, because the handcuffs really are on the money and the levers cannot fully pick that lock while most of them still land on the balance sheet or still need grant; where they were incomplete was in treating the tax rate as the only place money and capacity enter the picture, and in treating Number 10 North as mere symbolism, because a year of legislation has quietly changed what a given amount of money and capacity can deliver and almost nobody has narrated that shift.

Burnham's singular gift is the narrative, the ability, as Peter Hyman put it, to offer agency where Farage offers victimhood, and right now that gift is pointed squarely at the vision, when it would do far more work pointed at the three frictions: make the balance-sheet cost of each lever explicit and reserve the scarce subsidy for what genuinely needs it, structure institutional capital as a multiplier on public risk rather than a substitute for it, and treat delivery capacity and the revenue crisis as the first-order deliverable, and "good growth in every postcode" acquires a mechanism, whereas leave it undone and that same mechanism seizes on the same three points every time. The constraints are real, but none of these frictions are immovable, each has a remedy and a sequence, and clearing them in the right order is work a serious government can actually schedule, which is why I would end where the levers do: they are open, the frictions are named, and the task is to clear them in sequence, a harder and more honest promise than doubling down on a slogan.

Confidence and sourcing note. The statutory points (the SDS duty, CPO and hope-value reform, MDCs and MDOs, the HRA cap abolition, 100% Right to Buy retention, the National Housing Bank, the National Wealth Fund and the LGPS local-investment mandates) are grounded in the current instruments, but this is a part-commenced regime, so commencement duty will be needed to verify quantum against the latest position before relying on any single figure in formal advice. The £19bn finding, the Hartlepool per-head figures and the 6/14/24/32% tax comparison are as cited on The Rest Is Politics ep.548 and are attributed rather than independently asserted.