The money is ready. The places aren't. That's the real infrastructure story.

Why the £725bn moment will be won on the demand side and why most places are preparing for the wrong problem.

There's a comfortable story going around about UK infrastructure right now (See my blog from UKREIIF), and it goes like this: the scaffolding is finally up. A £725bn ten-year strategy. Two major Acts to reform planning and local government devolution on the statute book. A national project pipeline you can browse online. Pension capital pushed, by accord and by consolidation, toward exactly the long-dated, inflation-linked assets that places need. Put it all together and the conclusion writes itself the capital is coming, so get your projects on the list.

It's a good story. Most of it is even true. But it's the noise, not the signal.

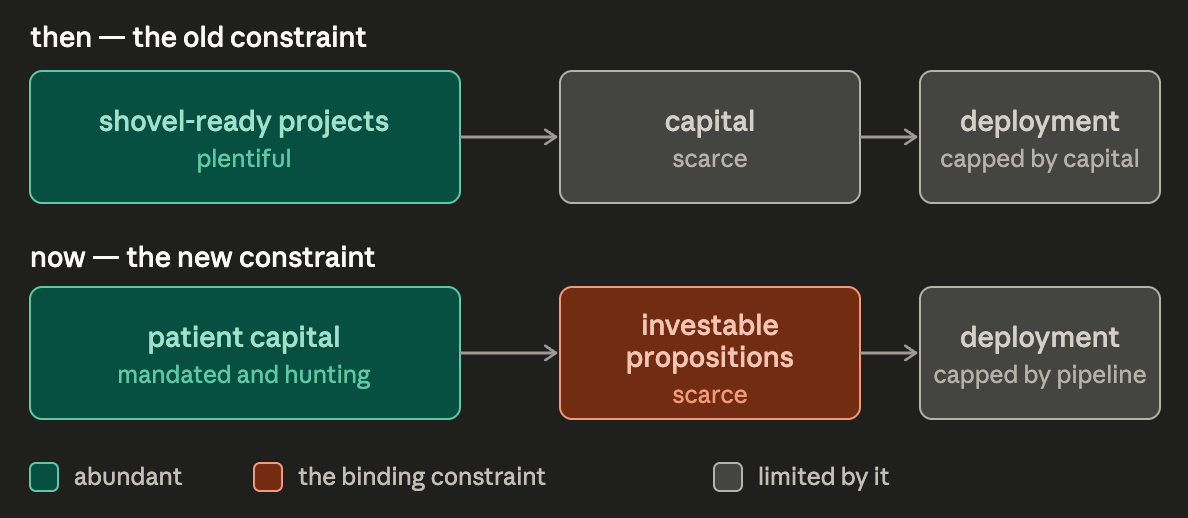

The signal is quieter and more inconvenient: the binding constraint on place-based infrastructure has moved. For a decade the honest complaint was that there wasn't enough patient capital looking for British infrastructure. That complaint is now largely obsolete. The money is mandated, pooled and hunting. What there isn't enough of is investable propositions and almost everything in the current policy conversation is built to solve the old problem rather than the new one.

If you're a place leader, a strategic authority, or an investor trying to deploy into local infrastructure, the difference between those two framings is the difference between wasted years and captured allocation. Let me make the case.

The genuine shift give it its due

I'm definitely not the sort person who waves away real progress, because the demand-side change is real and it's structural, and I have long championed a re-introduction of strategic planning, 21st century reform of both planning and local government, alongside better devolution to govern and steward the growth it can create a genuinely coherent and aligned demand for investment with proper long term and robust pipelines of investable activity across the built and natural environment.

On the supply side, large defined-contribution providers have collectively committed to move a meaningful share of default-fund assets into private markets this decade, with an explicit UK allocation inside that. Local government pension money is consolidating into a handful of large pools with the scale and mandate to write serious infrastructure cheques. The regulated-asset-base model the mechanism that quietly underwrites our energy and water networks by letting a regulator set a predictable return is being stretched into new territory, including nuclear and, before long, strategic roads. And for the first time there's a single public pipeline that lets global capital actually see the forward book of at sBritish projects.

Stack those up and you get a market where, at the aggregate level, capital availability is no longer the problem. Allocators are not short of money. They are short of things they can responsibly buy.

That is a profound inversion, and it is the most important thing happening in this space. It also quietly contradicts the advice most places are being given.

The misread: treating a demand problem as a supply problem

Walk into most "make our region investable" conversations and you'll hear the same prescriptions: produce a prospectus, bundle the projects, get listed on the pipeline, publish the data. All sensible. All necessary. And all aimed at visibility at being seen by capital.

But visibility was the old bottleneck. Being seen is no longer the hard part. Being buyable is. And buyability is a different discipline entirely, governed by questions a glossy prospectus rarely answers:

Who actually owes the money? Every clever financing structure for a local asset eventually rests on a payer. For genuinely local infrastructure that payer is frequently a local authority and after a run of effective-bankruptcy notices across English councils in recent years, institutional investors price local-authority covenant risk as a live concern, not a theoretical one. A revenue line is only as strong as the entity standing behind it. "We'll pay you for availability" means very little if the market isn't sure you'll be solvent in year nine.

Where does the cashflow actually come from? There's a world of difference between a revenue an economic regulator guarantees, a revenue a creditworthy counterparty has contracted to pay, and a revenue you hope materialises from future land value or avoided social cost. The first can sit at the senior, pension-friendly end of a capital structure. The last cannot not yet, and not without someone absorbing the first losses. A lot of place-based plans quietly assume the third kind of revenue can do the work of the first. It can't.

Is there a creditworthy, capable counterparty on the public side at all? This is the one nobody likes to say out loud. The new strategic authorities are, in many cases, weeks or months old. They are being asked to author institutional-grade investment propositions while still building basic commercial, legal and treasury muscle. The constraint isn't a missing document. It's missing capability and you cannot list your way out of a capability gap.

Does the proposition survive contact with scale? Allocators deploying at institutional size want large, relatively clean tickets. Place-based reality offers small, bespoke, heterogeneous bundles. Stapling a tram extension to a housing scheme to a heat network doesn't automatically diversify risk, done carelessly it correlates it, since all three ride the same local economy and the same political weather. Aggregation is an art, and most "bundling" advice treats it as a filing exercise.

And will the deal outlive the politics? Pensions are being asked to hold these assets for twenty years or more. That requires confidence that a revenue commitment fiscal, regulated or contracted will survive a change of government, a regulatory reset and a subsidy-control challenge. Durability is a feature investors underwrite explicitly. It is rarely something a place can offer by simply wishing for policy continuity.

None of these are reasons to be pessimistic. They are the actual job. But notice that not one of them is solved by getting on a list.

Why this is urgent rather than merely interesting

The reason this matters now, and not at some leisurely future point, is that allocation in a newly capital-rich market is a first-mover game.

When capital is scarce, everyone waits their turn. When capital is abundant but credible propositions are scarce, the places that can put a genuinely buyable, obligor-backed, revenue-certain bundle in front of an investment committee will absorb a disproportionate share of the available money and they'll set the template everyone else is then measured against. The places still polishing their prospectus while skipping the harder questions will find that the capital has been spoken for, by neighbours who did the unglamorous work first.

There's also a closing window on the policy side. Much of the enabling legislation is enacted but still phasing in through commencement orders and secondary regulation. The institutions are still defining their risk appetite. That's precisely the moment when a well-prepared place can shape how a structure gets used, rather than inheriting one designed around someone else's project. Early and credible beats late and polished.

So what does "doing the work" actually look like?

Here's where I'll be honest about what I'm not going to lay out in a public post because the method is the value, and because every credible proposition is specific to its place.

But I can tell you the shape of it. It starts by refusing to treat the investment case as a communications exercise and treating it instead as an underwriting exercise, interrogating each proposed cashflow the way an investment committee will, before the investment committee ever sees it. It means being ruthless about which assets in a bundle can carry private finance and which genuinely need grant or public first-loss, and saying so. It means engineering creditworthiness deliberately through the right wrappers, the right counterparties, the right sequencing of public and private capital rather than assuming a statutory power to charge is the same thing as a bankable revenue. And it means stress-testing the whole thing against the downside cases an allocator will run anyway, so that the answer to "what happens if the value capture comes in at sixty per cent of forecast?" is already on the table.

Done well, that work turns a place's ambition into something an institution can actually take to committee. Done badly or skipped it produces a beautiful document that no one buys.

This is the work I and my organisation have seen grow in demand on both the supplt and demand sides of place based investment, strongly driven by the pilcy changes in planning reform, accelerated devolution and perhaps a new understanding that a digital and data embedded apporach could actually be paradigm. This has really stimulated my ADHD rabbit hole interest in how we can laser focus (but with a systems lens) on helping places, authorities and investors close the gap between visible and buyable. Not by adding another strategy to the pile, but by pressure-testing the financing the way the market will, finding the blockers before an investor does, and structuring around them while the policy window is still open. If you're staring at a growth corridor, a regeneration programme or a regional pipeline and quietly wondering whether the money would actually show up that's exactly the question worth answering early, and properly.

The signal, one more time

The celebration is right that something has changed. It's just wrong about what. The achievement of the last two years isn't that the projects are ready — it's that the capital is. The places that understand the difference, and prepare for the demand-side problem instead of the supply-side one, will quietly take the lion's share of a generational wave of investment. The rest will wonder why being on the list wasn't enough.

The money is ready. The work now is making the places ready to receive it — and that work is more specific, more commercial and more urgent than the comfortable story admits.

If this resonates — or if you think I've got it wrong — I'd genuinely like to compare notes. And if you're wrestling with exactly this gap on a live programme, that's a conversation worth having sooner rather than later.

Signal over Noise — cutting through the infrastructure hype to the parts that actually move capital.